What should I know about REITs investing

What should I know about REITs investing

Low Soo Fang, from UOBAM’s Asia Equities Team, answers your questions on REITs investments going into 2022

1. Which types of investors may want to consider REITs?

A REIT (Real Estate Investment Trust) is an investment vehicle that invests in a pool of real estate assets. These assets generate revenue by collecting rent. About 90 percent of the profit, net of manager fees and other expenses, is then paid out to REIT unit holders on a regular basis.

So REIT investments are suited for those seeking sustainable and regular income that is potentially higher than bank interest rates or most regional government bonds. REITs are traded on the stock exchange so their unit prices can fluctuate based on market factors. This means REITs unit holders can also experience potential capital gains or losses.

Additionally, REITs have a relatively low correlation to other investment asset classes. So they are a useful diversification tool for equity and bond investors.

2. The worst of the Covid pandemic seems to be behind us. Is this good for REITs?

Many Asian economies are starting to recover from their lockdowns. Across the region and globally, we are seeing a pickup in economic activity and signs that GDP is growing again.

Typically, robust economic expansion translates into more demand for real estate, higher occupancy rates and therefore higher rentals and earnings for real estate companies. Economic expansion also produces higher inflation and typically, real estate owners are able to increase rent during times of rising inflation. So once there are clear signs of economic expansion, the real estate sector can be expected to benefit.

3. What about during periods of slow growth?

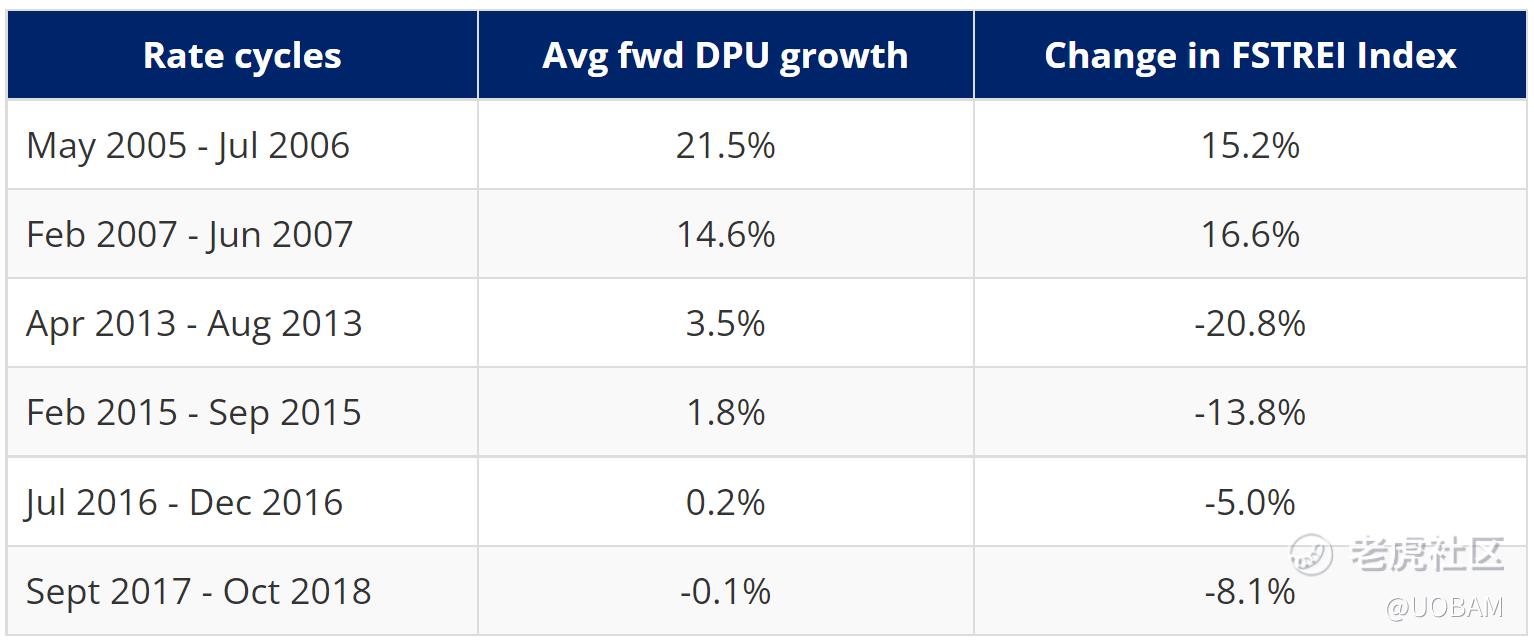

If we look at past episodes of US Fed tapering and how the REIT market responds, we can see a clear pattern. REITs tend to underperform during periods of slow growth and outperform when growth is on the rise.

For instance, in the US rate cycles between 2013 to 2015, a period characterised by low growth, SREIT (Singapore REIT) prices declined by 14 to 21 percent. The periods that coincided with near-flat DPU (Distribution Per Unit) growth saw milder declines of 5 to 8 percent.

On the other hand, during the 2005-2007 rate cycles when global growth was rising, SREITs gained 15 to 17 percent.

Figure 1

Source: UOBAM/Bloomberg

. Will REITs be affected if interest rates rise in Asian countries?

There is no direct correlation between REITs performance and interest rates. On the one hand, higher interest rates will tend to increase developers’ borrowing costs and lower property prices. It also makes REITs less attractive relative to interest payments from lower risk instruments such as fixed deposits and government bonds.

On the other hand, interest rates tend to rise when the economy is doing or expected to do well, as explained above. So it is important to understand the underlying factors that is pushing up interest rates. If interest rates rise in Asia due to healthy economic fundamentals, as we are expecting to be the case in 2022, then this should be positive for the REITs sector.

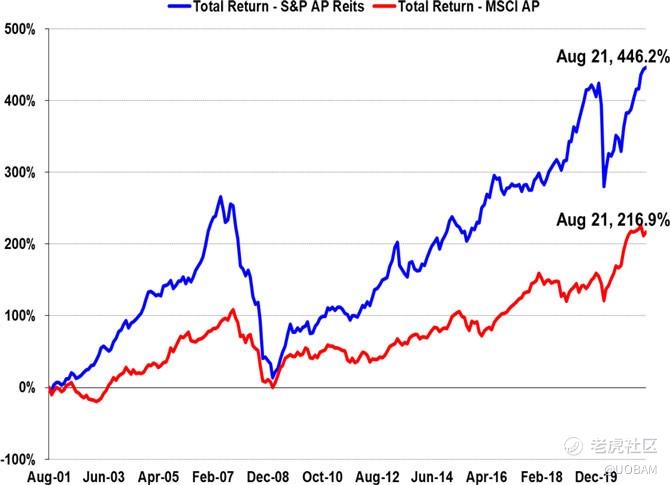

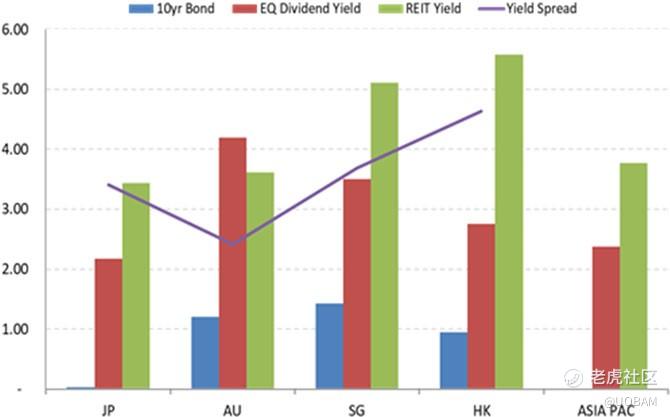

5. What is the outlook for Asia Pacific REITs over the mid and long term?

In Asia over a 20-year period, REITs outperformed bonds and equity markets, both in terms of dividend income and total return.

The average DPU yield for APAC REITs over this period was 5.9%. This exceeded equity dividend yields and 10-year government bonds yields. Similarly, the total return for APAC REITs was 10.3 percent per annum, compared to 7.3 percent per annum for Asian Pacific equities.

For 2022, historical trends suggest that APAC REITs performance may be choppy in the near term but should stabilise once there is confidence in the region’s growth prospects. DPU yields for the year are expected to be in the range of 4.0 to 7.0 percent, with an average of 4.3 percent.

Figure 2

Total Return: AP REITs vs AP Equities Aug 01 - Sep 21

Dividends: REITs vs Eq vs Govt Bond (as at Sep 21), By Country

Source: UOBAM, Bloomberg, as at 13 Sept 2021

6. What is the outlook for the different real estate sectors?

Among the different Asia Pacific REIT sectors, there are two that are of particular interest.

Office REITs are seeing structural changes to demand in a post-Covid world. However, the impact is likely limited in markets such as Singapore and Hong Kong where conditions are less conducive for a ‘decentralised office’ model. This sector also has a higher correlation to inflation rates and tends to be more cyclical in nature. Improvement in the macroeconomic outlook tends to be captured through rents with a shorter time lag.

We also note that the Asia Pacific Industrial REITs sector has the potential for strong earnings. We believe this is underpinned by demand for the buildout of a more resilient supply chain, in particular the re-shoring of manufacturing facilities. Year-to-date, the sector has raised additional funds in the equity and perpetual securities markets that will help fund new acquisitions and boost forward growth.

7. What is green real estate?

In recent years, there has also been increasing interest in real estate’s contribution to sustainability goals. More tenants are looking for buildings that offer attractive working and living environments. There is also a growing demand for properties that can limit their carbon emissions and save water and electricity.

As a result, these types of buildings have the potential to command higher rents. This has given rise to a growing investment focus on real estate with certifiable green credentials.

Important Notice & Disclaimers:

This publication shall not be copied or disseminated, or relied upon by any person for whatever purpose. The information herein is given on a general basis without obligation and is strictly for information only. This publication is not an offer, solicitation, recommendation or advice to buy or sell any investment product, including any collective investment schemes or shares of companies mentioned within. Although every reasonable care has been taken to ensure the accuracy and objectivity of the information contained in this publication, UOB Asset Management Ltd ("UOBAM") and its employees shall not be held liable for any error, inaccuracy and/or omission, howsoever caused, or for any decision or action taken based on views expressed or information in this publication. The information contained in this publication, including any data, projections and underlying assumptions are based upon certain assumptions, management forecasts and analysis of information available and reflects prevailing conditions and our views as of the date of this publication, all of which are subject to change at any time without notice. Please note that the graphs, charts, formulae or other devices set out or referred to in this document cannot, in and of itself, be used to determine and will not assist any person in deciding which investment product to buy or sell, or when to buy or sell an investment product. UOBAM does not warrant the accuracy, adequacy, timeliness or completeness of the information herein for any particular purpose, and expressly disclaims liability for any error, inaccuracy or omission. Any opinion, projection and other forward-looking statement regarding future events or performance of, including but not limited to, countries, markets or companies is not necessarily indicative of, and may differ from actual events or results. Nothing in this publication constitutes accounting, legal, regulatory, tax or other advice. The information herein has no regard to the specific objectives, financial situation and particular needs of any specific person. You may wish to seek advice from a professional or an independent financial adviser about the issues discussed herein or before investing in any investment or insurance product. Should you choose not to seek such advice, you should consider carefully whether the investment or insurance product in question is suitable for you.

Stay up-to-date with our latest investment insights Sign up now

免责声明:上述内容仅代表发帖人个人观点,不构成本平台的任何投资建议。

- LesleyNewman·2021-12-02that's interesting hahaha, but it's not my main investment. if I was biased towards technology companies, I would probably look at real estate, which is not on my radar点赞举报

- BlancheElsie·2021-12-02personally, I do not know much about the real estate industry, and the general trend of your analysis is quite correct, but it is not specific enough. I am looking forward to your next analysis.点赞举报

- BartonBecky·2021-12-02as far as I know, the real estate industry in this area is saturated and not that easy to invest in. so can you tell us more about your main business?点赞举报

- AgathaHume·2021-12-02of course,interest rates will rise, but that will only increase the cost of investing, and investment funds will become less attractive.点赞举报

- JackPowell·2021-12-02I would love to know if you could persuade me to overcome my fear of Omicron. if you can , I will buy in.点赞举报

- MariaEvelina·2021-12-02but the new virus made me hesitate, although I wanted to invest, but reason told me to wait. be patient hhh🤔🤔点赞举报

- yansuji·2021-12-02thank you so much for sharing. your analysis is very specific and accurate. I will understand and wait for an opportunity to do so点赞举报

- JudithGrant·2021-12-02investing in trusted real estate is indeed a good choice, I will continue to learn. this section is perfect for me.😁点赞举报

- BonnieHoyle·2021-12-02so do you see a massive economic recovery ahead? but I don't think so. Good luck点赞举报

- qqzhang·2022-01-12这篇文章不错,转发给大家看点赞举报