When it comes to investing in new fintech companies and the financing concept of BNPL— buy now, pay later — Affirm stock comes immediately to mind. So does its recent large price swings.

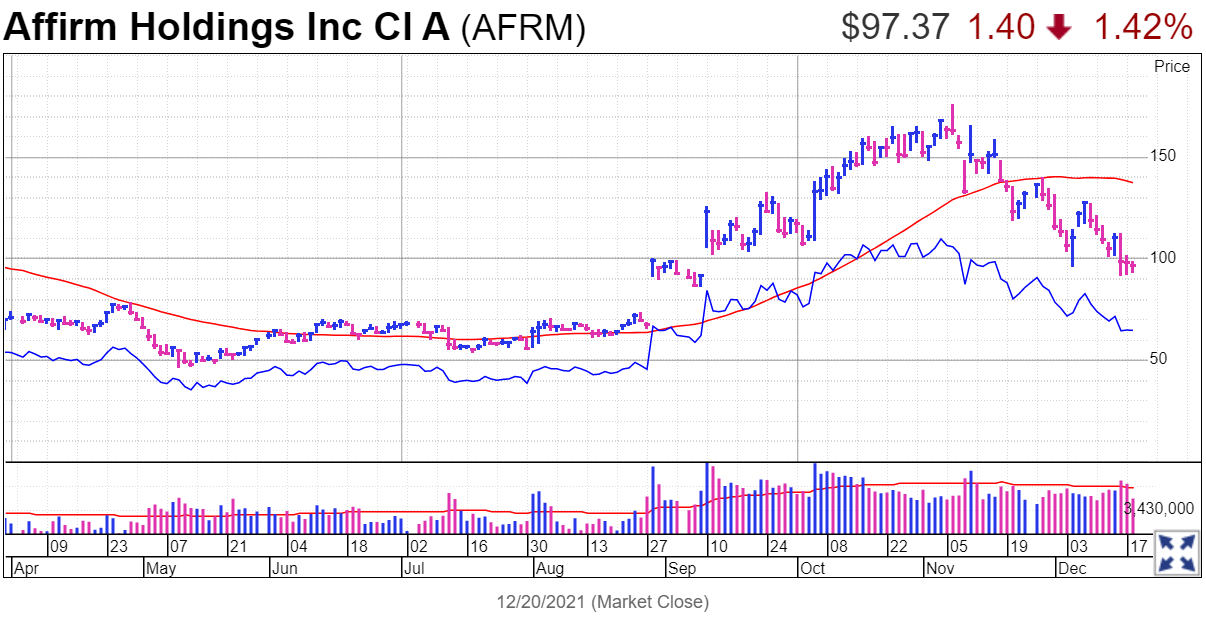

Affirm(AFRM) likely scared the wits of shareholders on Nov. 10.

The stock nose-dived 15% in the heaviest volume in more than three weeks. And 22.5 million shares exchanged hands that day, 42% above its average turnover over the past 50 sessions.

But after reporting third-quarter results late that day, AFRM went into bungee cord-jumping mode. Shares rose as much as 24% intraday on Nov. 11, then settled at 151.83. Good for a 13.7% gain. As the accompanying daily chart shows, volume soared again. This time, turnover bolted more than double its usual level.

Sellers are back in charge lately.

And after sinking more than 10% in heavy trading Thursday, AFRM fell another 2% after hours on news that the Consumer Financial Protection Bureau is conducting a probe of BNPL firms. Dow Jones reports that federal regulators are investigating Affirm, Klarna Bank, Afterpay and other competitors for the first time.

Yet before the recent sell-off, AFRM stock was showing troublesome technical action on its stock chart.

On Nov. 29, an early gain of as much as 2.5% melted into a disappointing loss of 3.5%. The stock clearly gotten turned away at a critical technical level on its chart,the 50-day moving average.

The fintech company, started by Max Levchin, entrepreneur and member of the so-called "PayPal mafia" of Silicon Valley fame, still sports an enviable gain of 97% from its initial public offering at $49 a share in January. However, AFRM shares fell hard recently on news of a convertible debt offering. Shares continue to test 100, a key psychological price level.

On Nov. 18, Affirm priced its $1.5 billion offering of convertible debt with a 0% coupon, maturing in November 2026. The zero coupon means note holders will not receive regular interest. Affirm says it may not redeem the notes prior to Nov. 20, 2024.

At $1.5 billion, it represented 4% of the total stock market value of the company.

Is Affirm Stock A Buy Now?

Should bullish investors in Affirm consider the current pullback a golden opportunity? Or given the big run-up already, is it actually a sell?

This story addresses aspects of IBD's CAN SLIM investment paradigm, coined by the legendary growth stock trader and founder of Investor's Business Daily,William O'Neil. So, we'll analyze the potential investment from multiple viewpoints: fundamental, technical and the quantity and quality of institutional ownership.

Without all three positive elements in place, a growth investor sports a smaller chance of reaping an outstanding market-beating gain over the long run.

Affirm Stock Today: The IBD Ratings Picture

IBD Stock Checkup shows Affirm's Composite Rating keeps falling, now at 32 on a scale of 1 to 99.

That score compares unfavorably with Affirm's industry peers in consumer credit and banking giants, includingAmerican Express(AXP) (a weakening 76 Composite score),Goldman Sachs(GS) (89 Composite) and Mastercard(MA) (70 Composite). Affirm's Composite also now trails a 44 rating for PayPal(PYPL), a struggling former member of IBD Long-Term Leaders and former member of IBD Big Cap 20.

Ideally, focus on companies with a 90 Composite or higher. However, newer issues often have no earnings history or a very slim record of profitability. For Affirm, the San Francisco-based company lost $1.75 a share in fiscal 2021, ended in June. The Street sees more net losses in FY 2022 (-$1.70) and FY 2023 (-$1.16).

According to MarketSmith, Affirm now has 281 million shares outstanding.

On the positive side, Affirm is growing the top line at lightning pace; revenues have grown 86%, 89%, 120%, 98%, 57%, 67%, 71% and 55% vs. year-ago levels in the past eight quarters. In the September-ended quarter, the top line hit a record $269.4 million.

"Legacy payment options, archaic systems, and traditional risk and credit underwriting models can be harmful, deceptive, and restrictive to both consumers and merchants," the company wrote in its 424b IPO prospectus, filed with the Securities & Exchange Commission." We believe that they are not well-suited for increasingly digital and mobile-first commerce, and are built on legacy infrastructure that does not support the innovation required for modern commerce to evolve and flourish. Our platform is designed to address these problems."

The company charges zero late fees. As of June 30, Affirm counts at least 10 million customers.

In its Nov. 10 news release on September fiscal Q1 results, Affirm noted an 84% boost in gross merchandise volume vs. a year earlier to $2.7 billion. Active merchants soared from 6,500 to 102,000, due in large part to the adoption of Shop Pay Installments by merchants on Shopify's platform. And active consumers grew 124% to 8.7 million.

Affirm's Relative Strength Rating is trying to stabilize at 80 on a scale of 1 to 99. Translation: AFRM is still outperforming 80% of all companies in the IBD database over the past 12 months. Now, keep in mind that AFRM has not yet traded a full 12 months. But the RS Rating also places extra weighting on three-month price performance.

According to MarketSmith data, the 3-month RS Rating shows an unsavory score of 6.

Mutual fund ownership keeps rising fast. The total has jumped to as high as 342 funds at the end of Q3 this year vs. 255 in June. Bullish. You want to see increasing institutional sponsorship. That's one hallmark of the I in CAN SLIM.

When investing in a growth stock, make sure it has solid company. Does it belong to a leading sector in the stock market itself? You can see the top performing sectors on a daily basis within IBD's stock research tables via IBD Data Tables.

Overall, that's pretty much the case for Affirm. While its credit card payment and processing industry group ranks in the bottom half of 197 IBD industry groups for six-month price performance, the finance sector currently ranks just outside the top 10 among 33 sectors in the IBD stock research tables at Investors.com.

Affirm Stock: Proper Buy Points

Soon after going public on the Nasdaq, Affirm's stock price corrected in a huge way after its breakout attempt past a 138.08 correct buy point in anarrow IPO base imploded. As you can see on the daily chart, in early February the large cap failed to get much traction after clearing the base's left-side high of 137.98.

Then it tanked just days later. This negative price action triggered the golden rule of investing: cut your losses short. By saving precious capital, you insure the portfolio from a devastating loss. And you ensure the opportunity to invest in a better stock or the same stock in stronger market conditions.

For Affirm stock, the new opportunity came in September.

After falling as much as 68% from its 146.90 peak, AFRM bottomed out at 46.50 in May, then began to rise slowly. It took months for the stock to begin building the right side of a promising new chart pattern. But it eventually crossed above the 50-day moving average and stayed above it.

On Aug. 30, shares gapped up in bullish fashion. A 46% gain in the heaviest volume in the stock's history catapulted Affirm to a five-month high, thanks to a business tie-up with an e-commerce titan. The next several days saw the stock tilt lower in mild fashion. Volume was still heavy, but declined from the mega-active day of Aug. 30.

This constructive price action created a handle on the deep cup.

View a handle as a final shakeout of uncommitted, weak shareholders. Those shares move to firmer hands. The handle clears the deck for a breakout — that is, a strong move to new highs once fresh institutional demand crowds the market for Affirm stock.

AFRM Stock: Round-Trip Sell Rule

On Sept. 10, Affirm stock broke out past the handle buy point of 101.10 on second-quarter results. Volume surged again. This move stoked AFRM's first breakout and legitimate buy opportunity.

Two separate pullbacks in September and early October created additional handle entries. Why? AFRM was still trading beneath the deep cup pattern's left-side peak of 146.90.

Thus, new entry points at 126.56 (10 cents above the Sept. 10 peak) and 133.27 (a dime above the Sept. 24 high) gave traders another timely chance to buy on strength.Always buy within the 5% buy zone after a breakout.

However, the current downdraft has resulted in a round trip of gains from these latest buy points. This action brings up one important IBD sell rule: Do not allow a superb gain of 10%, 20% or more turn into a loss.

A Future Follow-On Entry?

A fresh pullback to the 50-day moving average, or to the 10-week line on a weekly chart, normally offers a follow-on buy point after a successful breakout. In such a situation, you want to buy as close as possible to the actual 50-day or 10-week itself.

The 10-week moving average recently climbed to as high as 143. Buying within 5% to 10% of this price level is acceptable — but only if IBD says the market is in a confirmed uptrend. You want the market acting as a tailwind, not a headwind. And you want to see the stock rallying first. But AFRM has now closed four straight weeks below its 10-week line.

So at this point, Affirm stock is not a buy.

Ideally, you want to wait until the stock begins to rally again and clear the 10-week moving average with gusto before deploying your hard-earned capital. In other words, buy on strength, not on the way down.

Without question, Affirm stock has entered a base-building mode.

A continued drop through the 50-day line and the 10-week moving average spurs another defensive sell rule to lock in profits. After all, AFRM has made an impressive short-term rally, up 160% from its Aug. 27 close at 67.90 to its all-time high of 176.65 in less than 11 weeks.

For now, AFRM still holds above its recently formed 200-day moving average. A break through this long-term technical level would make the current slide even more bearish.

And most importantly? After any new buy, be sure to manage risk appropriately.Keeping losses manageable, ideally at no more than 8% from your purchase price, allows you stay solvent and in the game. It's far easier to recover from a 7%-8% loss than a 25% or 50% deficit. Given AFRM's heavy price volatility, you can also structure your position so that even a 10% loss does not result in more than 1% hit to the overall portfolio.