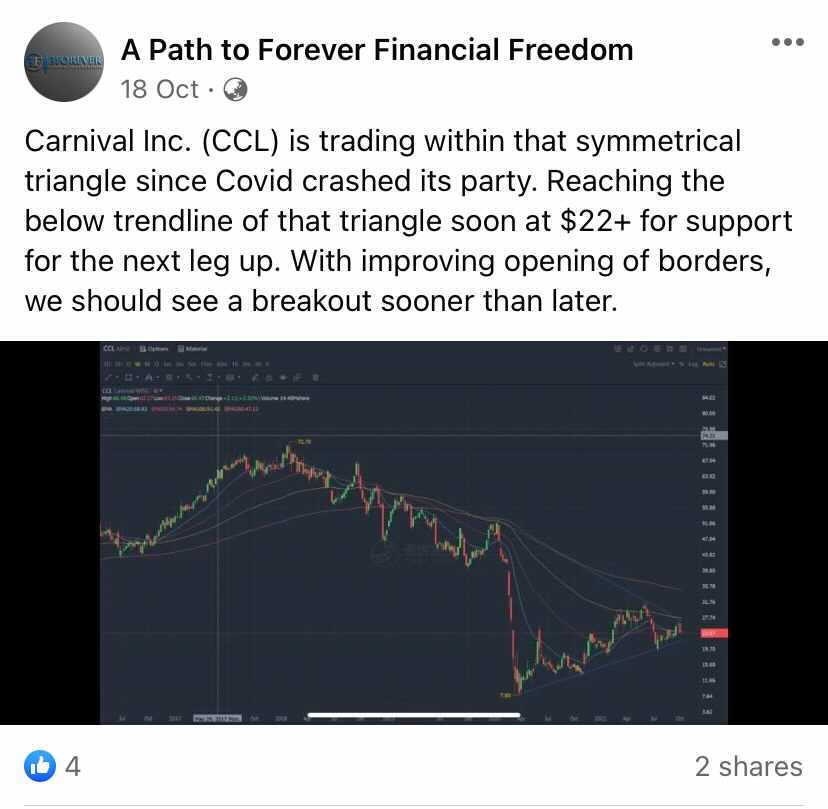

On the 18th October, I alerted the members in my Facebook group some technical charts for Carnival Inc. $Carnival(CCL)$

The price action is trading within the symmetrical triangle since COVID started back in early 2020 and hasn't been able to break in or out of that triangle since. Nevertheless, we are approaching that breakout (up or down) soon and may be able to know soon enough.

I went on to dig a few more information soon after that, in preparation for due diligence on its fundamental side.

I didn't quite like what I see based on the information I dig out so I'm likely to sit this one out for anything long term. This is at best a trading play on the sentiments if I just want to get my hands dip in a little for fun purpose.

Nevertheless, here's what I found out if you are still interested to read on.

Market Capitalization ≠ Enterprise Value

First, I wanted to establish this understanding between market capitalization and enterprise value.

While market capitalization and enterprise value are both measures of a company's value, the two are not identical and it is important that investors determine what is the devils inside the details.

Market Capitalization is the total value of all the outstanding shares of the company's stock. It is simply calculated by multiplying the stock's current price and the number of shares outstanding. That is it.

It doesn't take into account the capital structure of the company and how much the debt or cash the company carries in their balance sheet.

In comparison, enterprise value is a more accurate measure in the eyes of a true investor because it takes into account the consideration of its debt obligations.

The formula goes like this: Enterprise Value = Market Capitalization + Debt - Cash.

This is particularly valid in our case today like Carnival which carries plenty of debt obligations in their book since COVID hits them hard.

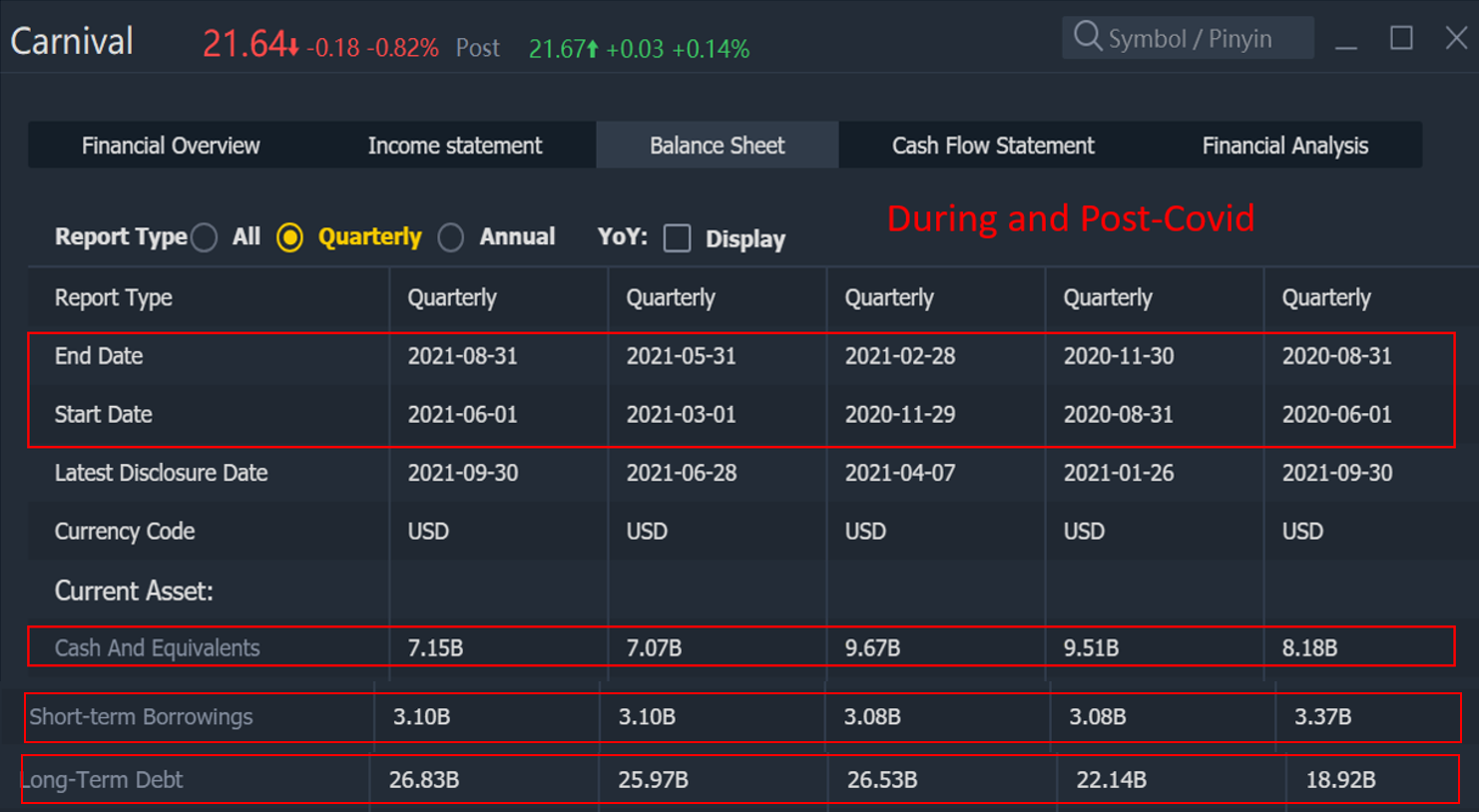

Carnival’s Capital Structure Has Greatly Changed Since COVID

The capital structure of Carnival Inc. has greatly changed due to COVID as the company has raised funds in the capital market for more than several times in both debt and equity.

Just take a quick look at this debt/equity ratio since COVID struck before I show you the details.

KABOOM!

The amount of new debt issued every quarter is just astonishing as the company tried to stay afloat.

If we take a look at the last 5 quarters of earnings results, the company has seen cash equivalent deteriorated by a negative CAGR of 12.5% per annum while both short term and long term debt increased by a CAGR of 31.8%.

That is not good by any company in the world standard.

What we want is to see in a good company is cash eventually going up (or it can decrease if they decide to use it to acquire or do share buyback or dish out higher dividends but they are all for the good wellbeing of the shareholder) and debt going down, not the other way round.

But it is understandably so, as the world has not fully returned to normalcy and recovery is still underway.

If we take the last closing price as of 28th October 2021, the company has a MARKET CAP value of $24.3B.

It’s ENTERPRISE VALUE however, is at your market cap + debt – cash, which in this case is $24.3B + $29.9B – $7.2B = $61.4B.

When comparing for valuation multiples, you would ideally want a lower enterprise multiple than a company with a higher enterprise multiple. This is measured against your denominator of EBITDA.

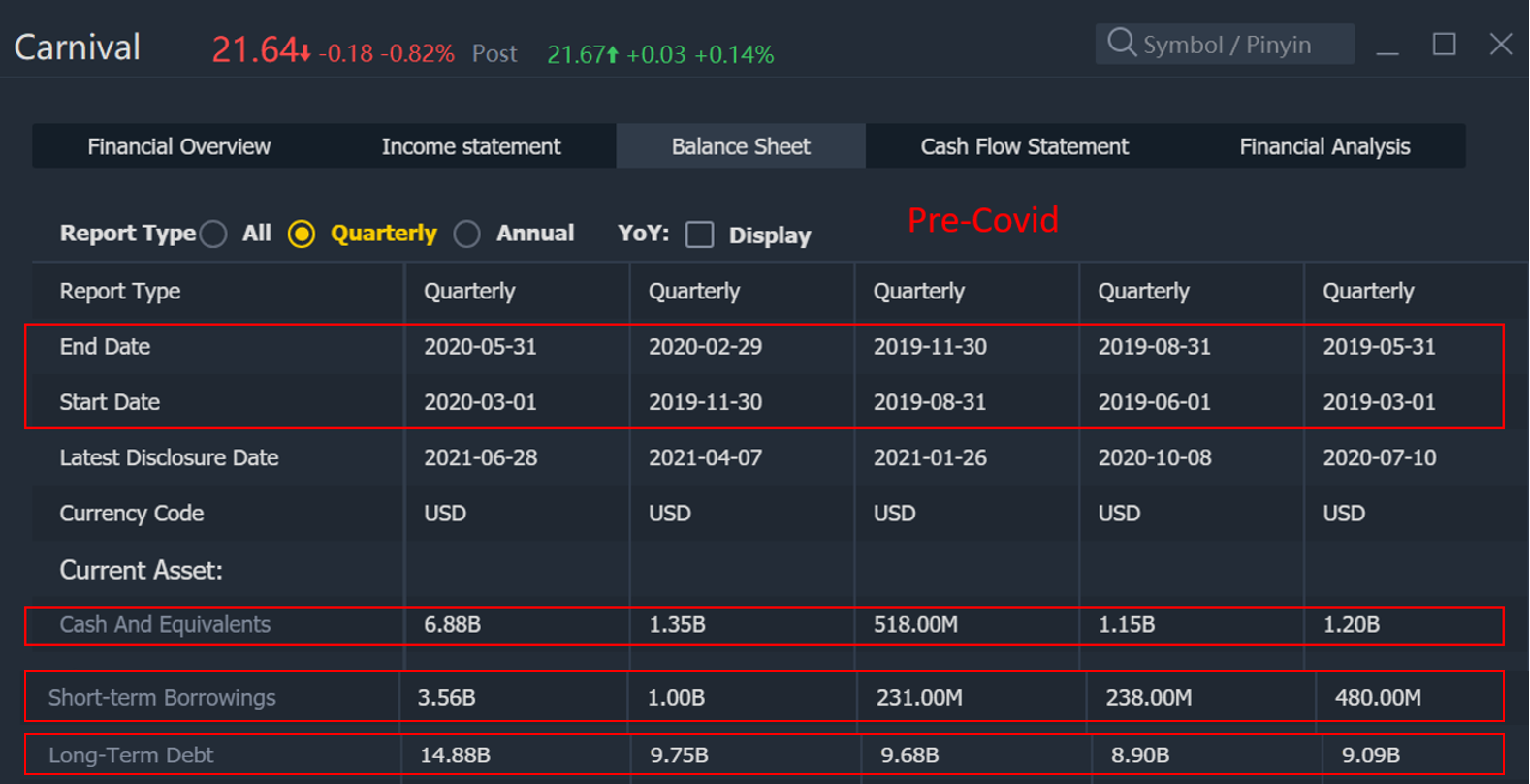

If we compare this against how the company fares before COVID, this paints a different picture.

If we look at the balance sheet of the company back in 2019 before COVID hits us, it has a cash equivalent of around $500m-$1.2b.

The total debt obligation is much lower than what it is today at lesser than $10b.

Using the market cap of $35b, it has an enterprise value of $35b + $10b – $500m = $44.5b, which is significantly lower than what it is today.

Recovery is under way but company is still burning cash

There is no doubt that recovery is under way and we should be seeing better days ahead for the company (and the world!).

There is also no doubt that consumers will continue to re-engage with cruising (once a doubt during COVID) as there is still very strong demand for it.

But if we are looking at real recovery from the numbers point of view, we are looking at years away.

Just take a look at how much cash they are burning for each quarter and you get the idea why they need to keep raising for new debts each month.

Even as the company reported $630m in customer deposits for booking in the Q3 FY2021, we are still looking at negative cashflow overall and a faraway to breakeven cashflow.

Conclusion:

The recovery years ahead means that we are probably off the worst already for the company and the market is pricing in a higher low and higher high over the past few months to indicate that.

We may continue to see the stock moving higher over time as we get better news on the vaccine situation and a decreasing plot ratio of infection. In fact, if we look at the other industries affected similarly, most of them had exhibited the same trend.

But the takeaway I want to make here is that Carnival Inc. is not the same company as it was before the COVID even if the share price goes back to it's pre-COVID days. This is because from a capital structure point of view, it has changed tremendously and the company is now carrying a huge sack load of debt obligation more than before, and as a prudent long term investors, it means you are not likely to get a good valuation on this company anytime soon, not until years away.

www.3foreverfinancialfreedom.com

精彩评论

How you get 61.4

Anyway i see your point. Thanks for sharing

1 year Carnival Corp. Forecast: 48.90

5 year Carnival Corp. Forecast: 250.842 *