Is Apple overvalued now? Is it a good buy?

With Apple Market Cap hitting 2.5 Trillion USD, I am sure these questions are in your mind.

Here are my key takeaways:

-With 94.77 Billion Free Cash flow for Trailing-Twele Months, current valuation of Apple could be 260 USD per share with a Discount Rate of 5% and Growth Estimate of 5% for the next 10 years.

-Apple has the strongest MOAT among all smartphone producing companies, which is 20% of the global market share.

-Apple's profits have grown at 9.6% yearly for the past 5 years. Free Cash flow has grown at a CAGR rate of 9.4% for the past years. Share buybacks has increased from 33 Billion USD in 2017 to 72 Billion USD in 2020.

-Apple is currently working on launching Apple Cars, and its rumoured to began production by 2024. With the Tech and softwares that apple has, I am sure their cars will beat Tesla.

-Sales and revenue of Apple is strong. With new products and constant investment into R&D, Apple is has become a brand status for everyone.

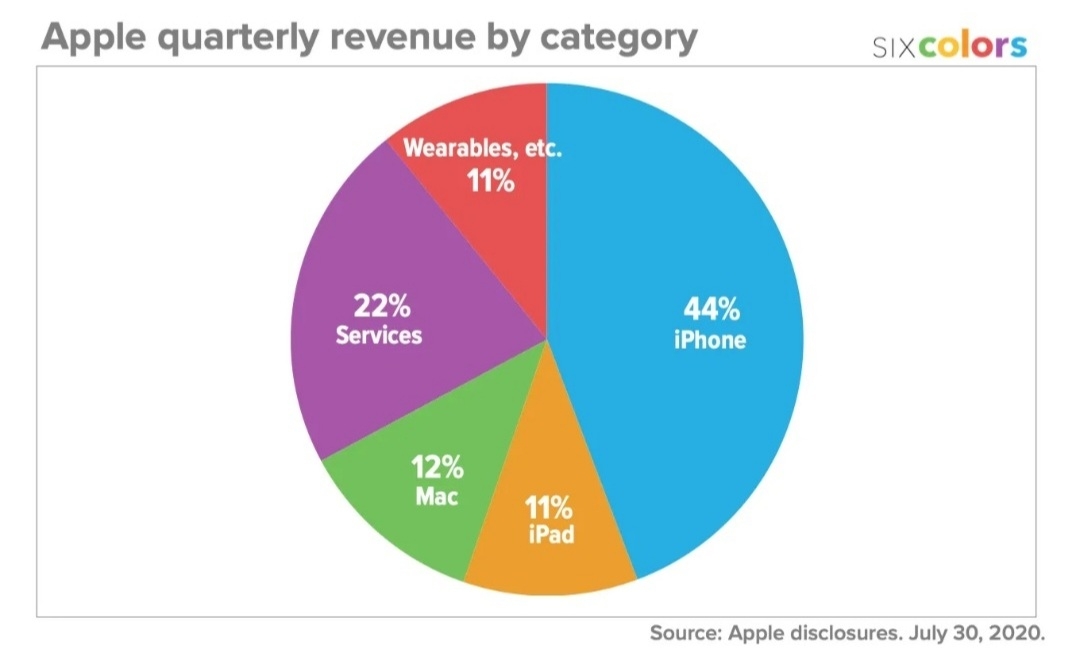

-Apple largest contributor of revenue is Iphone which is at 44%. The second biggest is Apple's services which brought it 22% of revenue followed by 24% for ipads and Macs and 11% for weareables.

-Warren buffet holds 5.4% of Apple Shares outstanding, and its the biggest holding of his Berkshire Hathaways Portfolio at 44.6% . If Buffet himself would bet a 44.6% stake of his portfolio into this company, investors can be assured that it is a solid company.

My key Takeaways:

-Apple is a great company, with a strong fundamental Moat. The greatest in the world in fact.

-I would buy, as I can foresee Apple taking more market share in the coming years. (Expected to take 40% of market share by 2024)

-With new rollouts and new projects in apple, more revenue is expected to be brought it in the voming years.

Conservative Valuation: 150-160 (Fairly Valued)

Aggresive Valuation: 200-260 (Undervalued)

What do you guys think? Let me know!

精彩评论