各位好,我刚加入这个平台目的就是要写文章。内容会很丰富但最终还是围绕着投资和密码货币这个范围。希望你们会喜欢我的作品。喜欢的话可以给我点赞,好评或可以在你的朋友圈分享给其他人阅读这篇文章。多谢支持!

如果你有某个内容想要我写,可以在评论里留下留言。谢谢!

There are only that much investing and financial tips I could share here. In order to speed up your understanding to invest safely with a well maintained portfolio allocation across asset classes, it will be of best interest to share real life examples of what people are going through so that we can minimize making the same mistakes.

Disclaimer: All information stated below are only for illustration purposes. Its not a call to buy or sell any financial products. As always, please perform your own due diligence before investing.

Here, I will share the first real life example of the following issue that this person is facing. To read the original post, click on the link here.

https://seedly.sg/posts/i-have-a-messy-portfolio-help-please?utm_source=telegram#_=_

Background Analysis

He/She is working for a few years and emergency funds have been set aside. This shows that this person has planned and set aside extra savings for the sole purpose of investing.

With that in mind, he/she will probably not be pressured into making irrational decisions and go cut loss or sell the investment assets when the bear market comes or prices of assets drop.

The only pressure comes from the fact that he/she is planning for marriage, purchasing of first home, and family creation where a substantial amount of cash is required to be paid in about 2 years.

With a 2-year horizon, it’s still possible to take some risk in investing.

Main issues with his/her existing investing strategy:

Disclaimer: there will be some assumptions that I undertake to analyze this investment portfolio

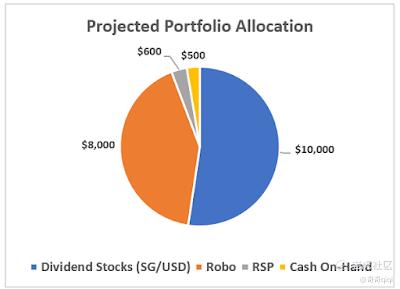

10K SGD invested in a few RANDOM stocks in SG and US market using Saxo platform. When you invest in random stocks, you will likely get random returns as well, no joke. 😅 He/she mentioned that the stocks are mainly dividend stocks, means that their prices tend to remain the same over the long run and do not have much capital appreciation. Your returns are mainly contributed from the dividend yields percentage of each stock.

8K SGD invested in 2 Robo-Advisors. This can either be two different plans in the same Robo-Advisor, e.g., a36% risk-level plan and a 10% risk-level plan both in Stashaway, or one plan in Stashaway and the second in Syfe for example. There’s likely some overdiversification in this strategy.

Regular Savings Plan (RSP) auto deposits 100 SGD per month to invest into STI ETF index for less than a year. In this case, I assume 6 months has passed, which is about 600 SGD into the plan.

Current cash on-hand only able to set aside low hundreds per month for investing. In this case, I assume low hundreds as a value less than 500 SGD per month.

Portfolio Analysis

I have personally bought and tried all the investments that this person has currently, so I am very familiar with the returns and what he/she is going through now.

Dividend Stocks

10K SGD in random dividend stocks in SG and US markets. Firstly, SG dividend stocks tend to have little price appreciation over the years. Their price increments are so small that its almost non-negligible.

To earn from holding onto these dividend stocks, the only way is through their dividend yield.

The first thing is to look at which stocks are performing and underperforming at the moment. If you see that dividend stock is what you still believe in for their returns, I will suggest to sell away those underperforming stocks (either you know that within this 2 years that stock will still be making a loss in price or to sell and buy into a current stock that you are holding to increase your overall stock position to get more dividend yield for the year).

Robo

Currently you are holding onto two different Robo plans. I would suggest selling one and focusing on the other. If you choose the most aggressive Robo plans in the market such as Stashaway or Syfe etc. and with the highest risk levels, their maximum return of investment is about 12 to 14% of what you have invested in. Any higher return is a bonus.

It does not make sense to hold onto two and it will only dilute your overall returns instead of diversifying your risk from holding the two Robo plans.

RSP (Regular Savings Plan)

If you have bought the RSP for STI ETF with DBS some months ago, I am making a calculated guess that with the recent rise in STI ETF prices, you are still making a price gain from your stock purchase.

I myself had purchased the RSP as well more than a year ago and held onto this plan for close to one year with a loss due to Covid 19. Now if you are still making some price gains in this plan, better to take whatever gains you have now and exit this plan while you can.

To find out more about my past RSP journey using the STI index, click on the URL below.

https://medium.com/the-investors-handbook/whats-the-issue-with-the-straits-times-index-sti-index-e719b2bd5454

Holding onto this plan will not help you much. If you are only depositing 100 SGD per month, you are holding onto very little STI stock shares. With so little shares, your monthly dividend yield return will be less than 4 SGD. In 2 years, the most you are going to receive for holding onto this RSP plan is about 96 SGD only (4 SGD x 24 months). Are you sure you want to do this for 2 years??

Moving Forward

What I would do in your shoes is as follows (do not blindly follow).

Strategy 1.1: Aggressive and risky for 2 years

- Exit the RSP plan (600 SGD)

- Exit the Robo-advisor (8k SGD)

- Exit the Dividend stocks (10k SGD)

- Cash on-hand (500 SGD)

- Open an crypto online account

Buy BTC/ETH cryptocurrency and park the coins into a high interest rate online exchange platform (gain both the price appreciation of the coin and interest rate per annum returns) eg. Blockfi, Celsius Network etc

These interest rate will keep changing so research and be aware before placing your order.

I have covered this in a previous article on how to earn simple interest using BlockFi. Click here to find out more.

https://medium.com/the-capital/crypto-yield-farming-part-1-2-195e1fd2e617

Strategy 1.2: Aggressive and risky for 2 years

- Exit the RSP plan (600 SGD)

- Exit the Robo-advisor (8k SGD)

- Exit the Dividend stocks (10k SGD)

- Cash on-hand (500 SGD)

- Open a CakeDefi account

Buy DFI coin and stake into the staking pool using the CakeDefi platform to earn estimated projected compounded interest of about *90% per annum. (*This will keep changing). There are many other AMM platforms out in the market. CakeDefi is one of them.

These interest rate will keep changing so research and be aware before placing your order.

If you have higher risk appetite, look into Liquidity Mining (LM) for higher gains than just normal staking. However, beware of Impermanent Loss when you deposit or withdraw your coins from the LM pool.

I have covered this in a previous article on how to earn compounded interest using CakeDefi. Click here to find out more.

https://medium.com/the-capital/crypto-yield-farming-part-2-2-e19d73aca30f

Strategy 2: Less aggressive and risky for 2 years

- Exit the RSP plan (600 SGD)

- Exit the Dividend stocks (10k SGD)

- Keep the Robo-advisor (8k SGD). Consolidate the two plans into one plan.

- Cash on-hand (500 SGD)

- Invest into an ETF

Invest and hold onto the S&P 500 ETF for the 2 years. Investing in an Index Fund will take up less time and resources to research and you don’t have to spend time to constantly look and study into individual stock picking.

It should be able to provide a slightly higher return compared to the RSP and dividend stock plans.

Above all of what have been shared, the issue is to highlight the overdiversification / overlap of investment within the multiple asset classes. Consolidation into just one or two investment assets will bring about better returns in the long run.

Originally published at https://medium.com/fortune-for-future/portfolio-rebalancing-learning-lesson-1-f5cf71663ef4

精彩评论