$KEPPEL DC REIT(AJBU.SI)$ has been one of the performing stars in the SREIT universe for quite some time since its’ IPO.

Investors who are looking to buy this REIT has been given very little to no chance to add on to their shares as the company continues to shoulder on its meteoric rise in the past few years.

Since hitting the peak of $3.13 sometime in October last year, the company has undergone quite a bit of correction over the past few months, breaking it’s support each time as it moves lower.

With the company trading at $2.34 today, is this a good opportunity to add on to the shares given their longer term prospect?

Maiden Acquisition in China with a high 9% NPI Yield:

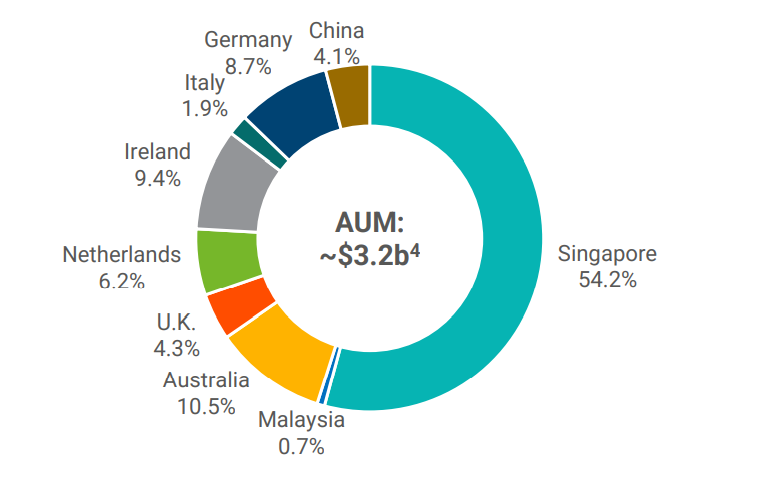

The maiden acquisition in Guangdong Data Centre located within the Greater Bay of China certainly provides a nice overall accretive bump to its overall earnings yield.

After all, we are talking about a net NPI yield of 9% which is funded via equity which at the time of the acquisition, it was trading close to P/NAV of 2x. DPU accretion as a result of the acquisition is expected to increase by about 2%.

Although the acquisition comes with a triple net basis sales leaseback for 15 years (increase wale), the land tenure is a leasehold with approximately 46 years remaining. Still, I do think the NPI yield of 9% for a data centre makes up for the shorter leasehold.

This deal is expected to be completed in the 2H of this year and should start contributing within the next reporting quarter.

Smaller Acquisitions in Europe and Sydney:

The company has been very active in making acquisitions and gaining traction in their footprint diversifying their bases outside.

Earlier in the 1H, they have completed the Intellicentre 3 acquisitions in Sydney for about $26m with a 20-year triple net master lease agreement for a freehold asset.

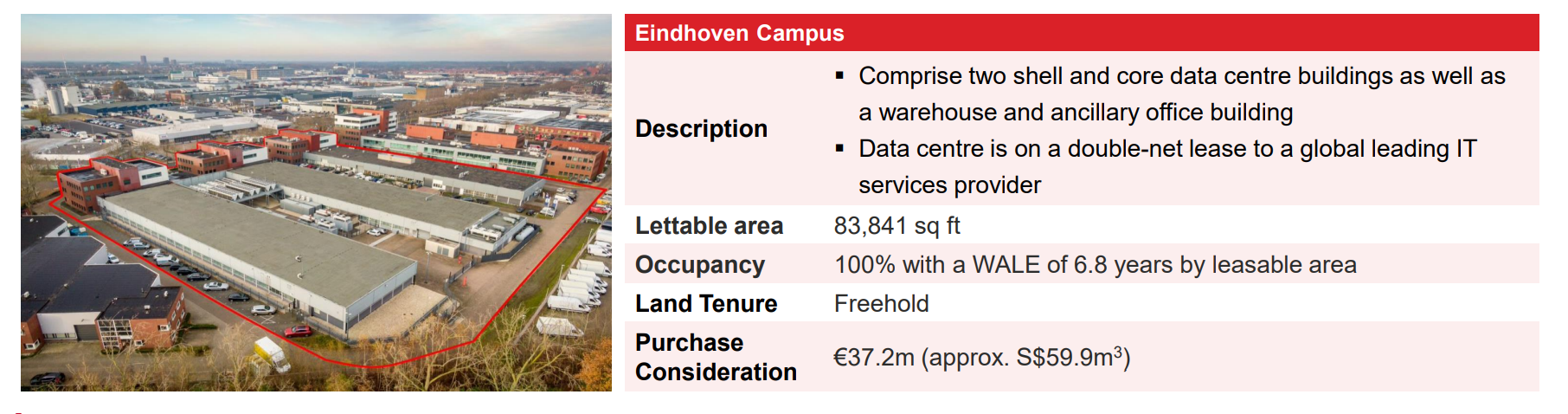

Recently earlier this month, they have announced another acquisition for a data centre building in Eindhoven campus, Netherlands for another $60m acquisitions. This comes with a 6.8 years of WALE on a freehold piece of land that is expected to increase and boost its DPU further.

Technical Chart:

From a technical chart view, I like what I am seeing in the chart.

On the weekly chart, the share has been respecting the EMA100 support (yellow trendline) for a long time and has rebounded off the support for more than 4 times in the past 4 years, including the big one during the Covid-19 pandemic.

However, it recently broke this strong support and is now likely to head down to the EMA200 at $2.15.

This translates to an annualized yield of 4.5% and probably even more if we consider the upcoming acquisitions in China and Netherlands once completed.

I’ll likely wait for this level to park some of my money for the longer term portfolio.

精彩评论