On August 20th last week, Snowflake$Snowflake(SNOW)$ plunged 11% in intraday trading because of a report by Cleveland Research. Snowflake's new signing growth is slower than in the first quarter, while consumption growth is likely to be flat at most in the first quarter, the report said. As well as increased competition from super enterprises, the company's sales cycle will be prolonged.

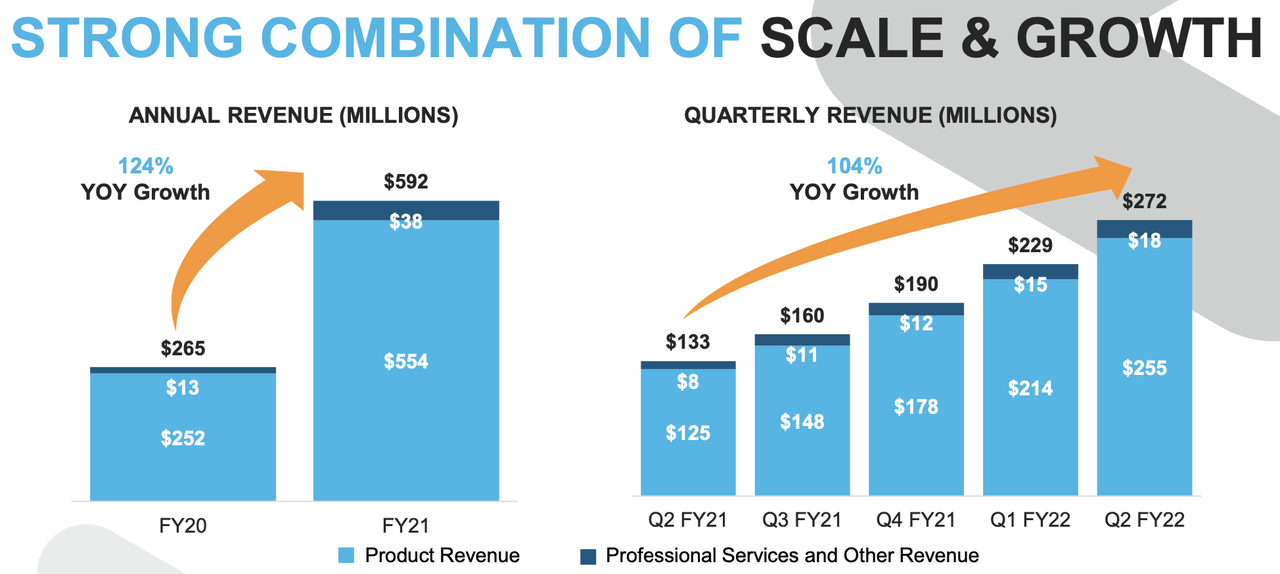

And specifically, looking at this financial report,people have always had strong performance expectations for Snowflake. In this quarter, SNOW's revenue of US $272 million increased by 104% year-on-year, maintaining a high triple-digit growth.

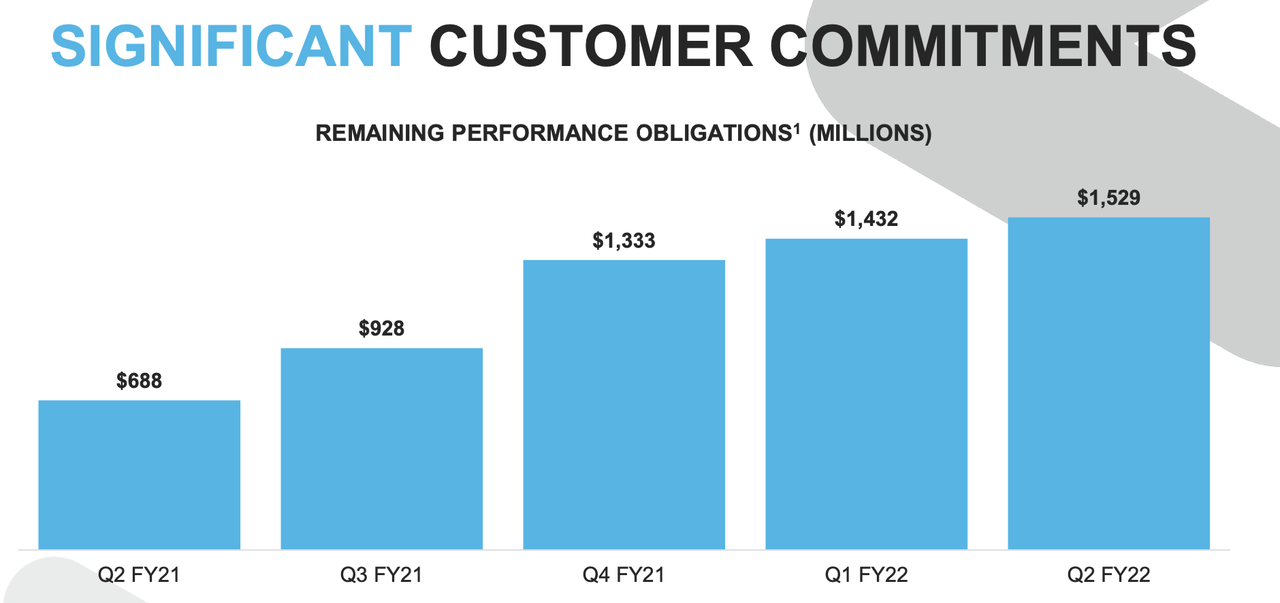

Importantly, the residual performance obligation (RPO), which represents future unearned income, also performed strongly, with a year-on-year increase of 122%.

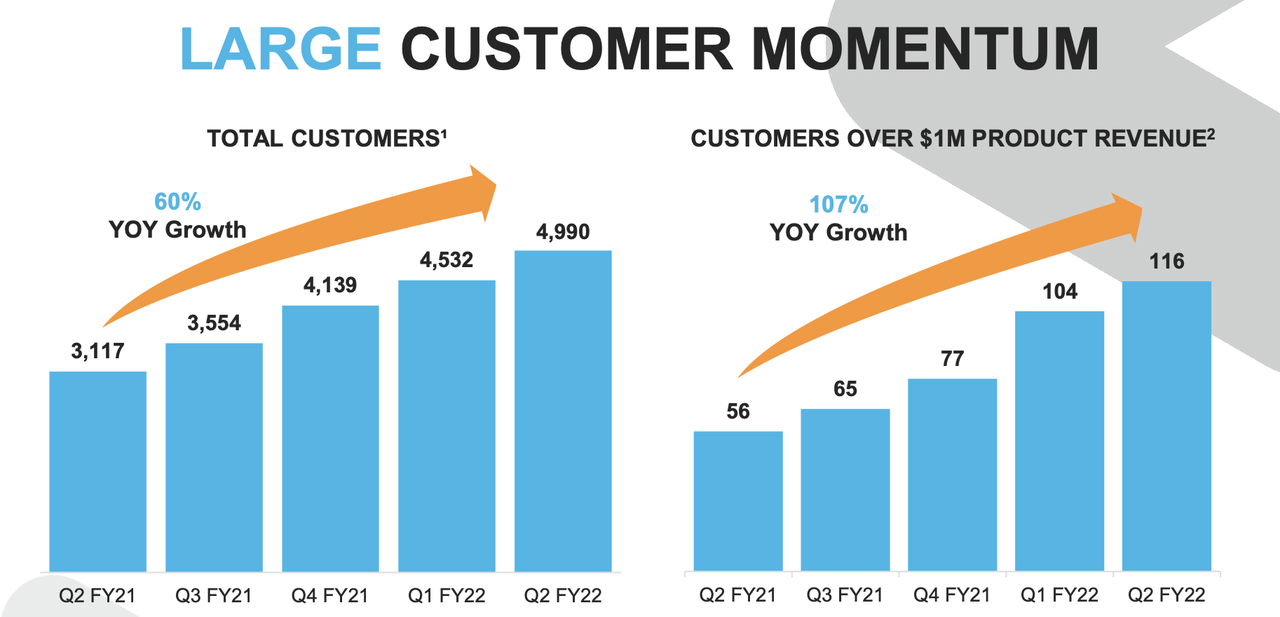

SNOW's high growth is also reflected in two aspects. First, its total customers increased by 60% year-on-year.

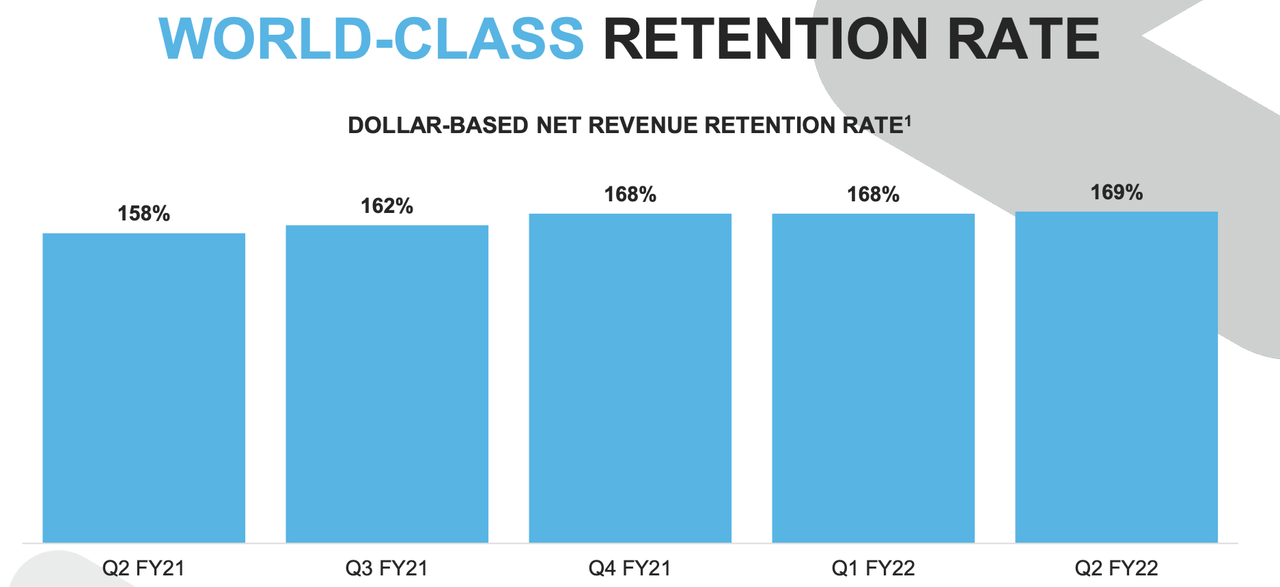

Secondly, and most importantly, 169% of NRR is the best of its kind.

That means Snowflake's consumers spend an average of 69% more on the company's products than they did last year. An important reason for this strong performance is that SNOW adopts a consumption-based mode of charging instead of a fixed subscription fee. This gives customers the flexibility to dynamically increase usage and allows SNOW to directly share the data growth dividend. As SNOW customers generate and analyze more data, SNOW can make more money-it's as simple as that.

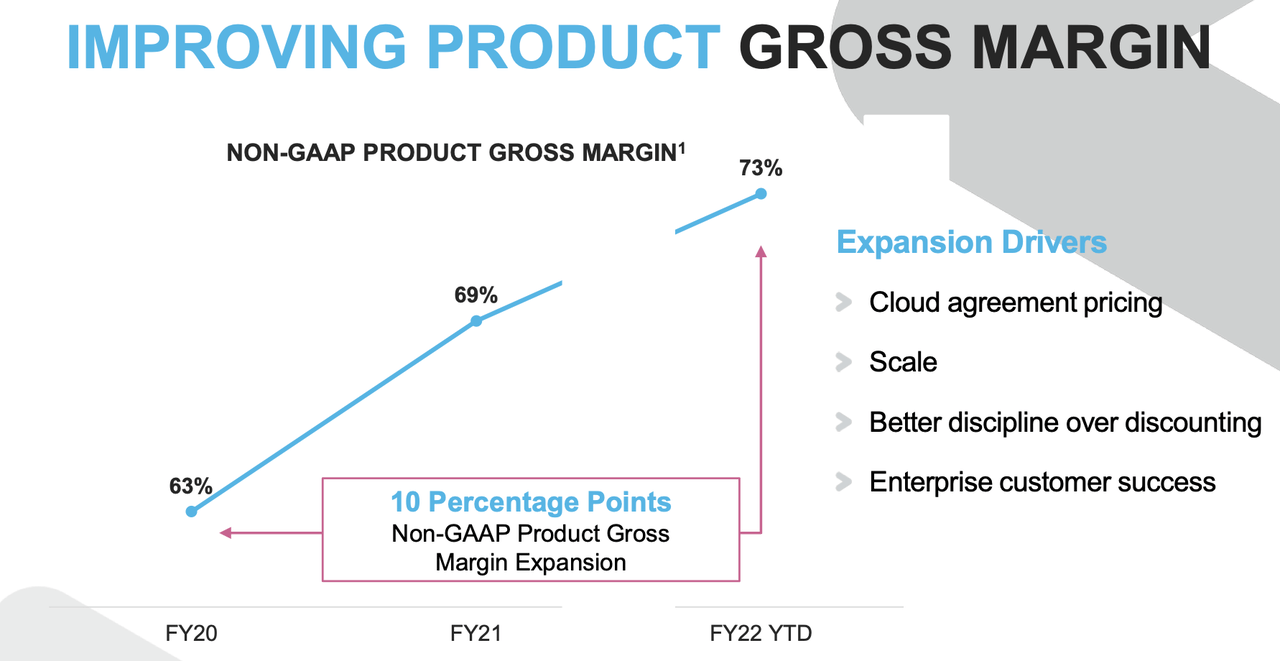

In addition to the typical strong growth, there are more positive factors in this quarter. SNOW's gross profit margin increased to 73%, up from 63% two years ago.

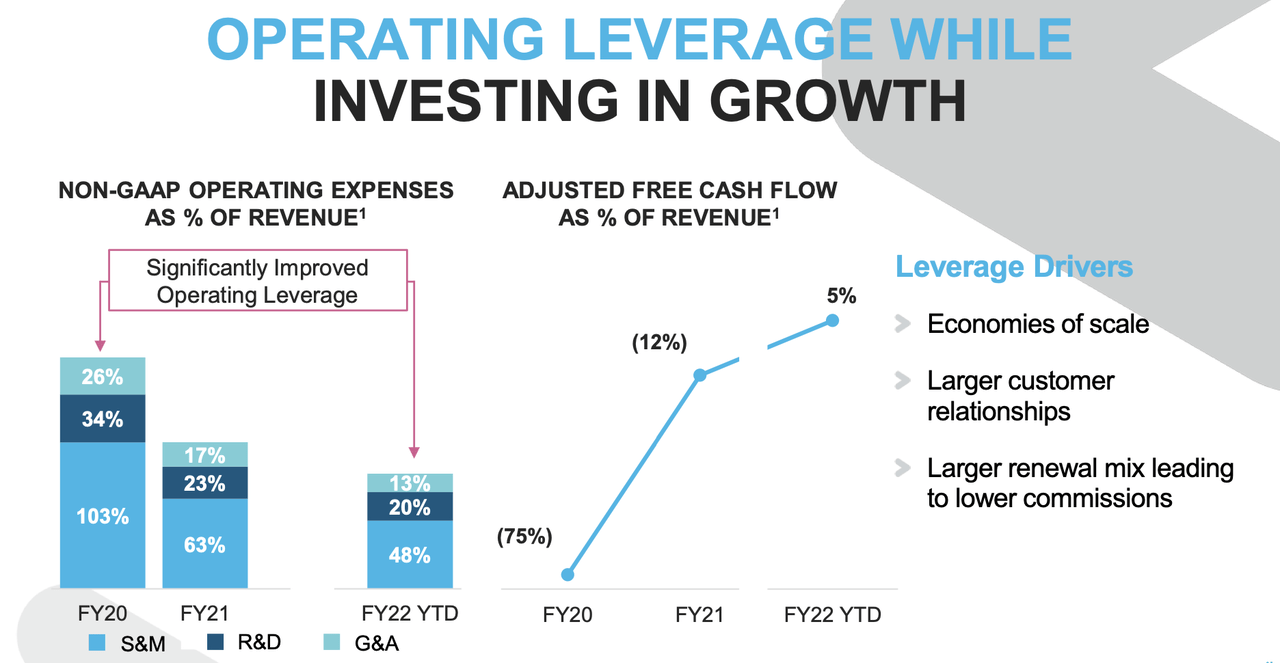

The improvement in revenue helped SNOW gain some operating leverage, because the company's free cash flow has been positive so far this year.

SNOW predicts that the revenue growth rate in the next quarter will reach about 90%, and the median annual revenue growth rate will reach 92%.

Always high valuationBuy or sell?

When you talk about Snowflake, you must talk about valuation. SNOW's current share price corresponds to 101 times the revenue of the past 12 months, which is a great valuation. However, if the company can maintain strong growth rate, it makes sense.

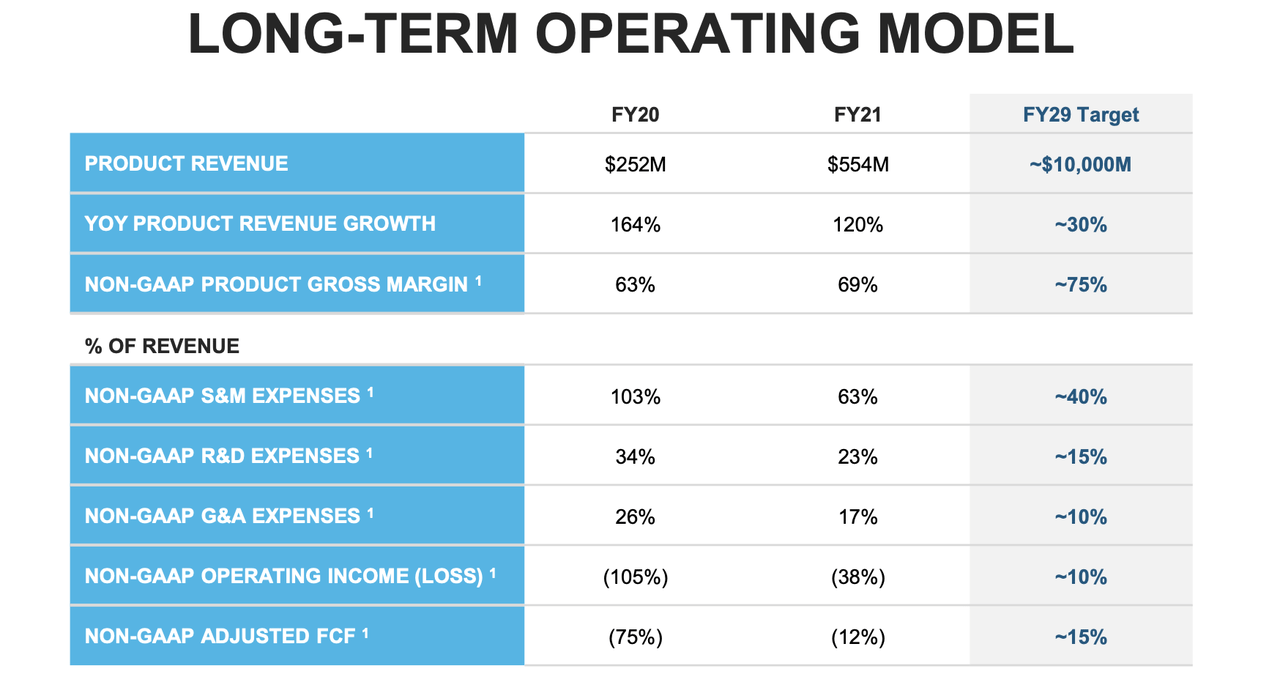

At this year's Investor Day event, SNOW expects product revenue to reach $10 billion in fiscal year 29:

Remarkably, the consensus on Wall Street, at least among the two analysts who have already predicted this number, is that SNOW will actually be $11.1 billion in size by FY2029.

That would be an incredible 892pc increase over revenue projections for the year. However, it is not clear whether it can provide huge returns to shareholders in such growth. SNOW guides Non-GAAP operating profit margin of 10% in fiscal year 29:

I noticed that GAAP's operating profit margin will be much lower due to equity incentive compensation. If SNOW really can only generate 10% Non-GAAP profit margin on the basis of $10 billion in revenue, there is some concern, because it is expected that the company will have achieved significant operating leverage by then.

Let's demonstrate this with a 30% long-term net profit margin forecast. If we assume that SNOW's price-earnings ratio (PEG) in fiscal year 29 is 2 times, then the company's price-earnings ratio is about 60 times and the market-to-sales ratio is about 18 times. By fiscal year 29, that is, seven years later, the valuation of the company's stock will reach 200 billion US dollars. SNOW expects the stock to be diluted by about 3% a year-let's use 2%. SNOW may have 348 million outstanding shares in FY 29, so its estimated share price may be $575. At current levels, the share price will rise by 102%, with a compound annual return of 10.6%. This rate of return may outperform the market, but there seems to be no obvious margin of safety. Such valuation assumptions already use aggressive growth and profitability forecasts, but such low annual returns could disappoint investors. Of course, this is only one of the linear predictions, and the reality is more complicated.$Snowflake (SNOW) $

精彩评论