$SINGAPORE PRESS HLDGS LTD(T39.SI)$

OBSERVATIONS

•SPH becomes a mostly Property co after removing Media biz

•Besides their stake in SPHREIT, they have assets in Nursing Homes, Student Hostels in UK & M1 stake

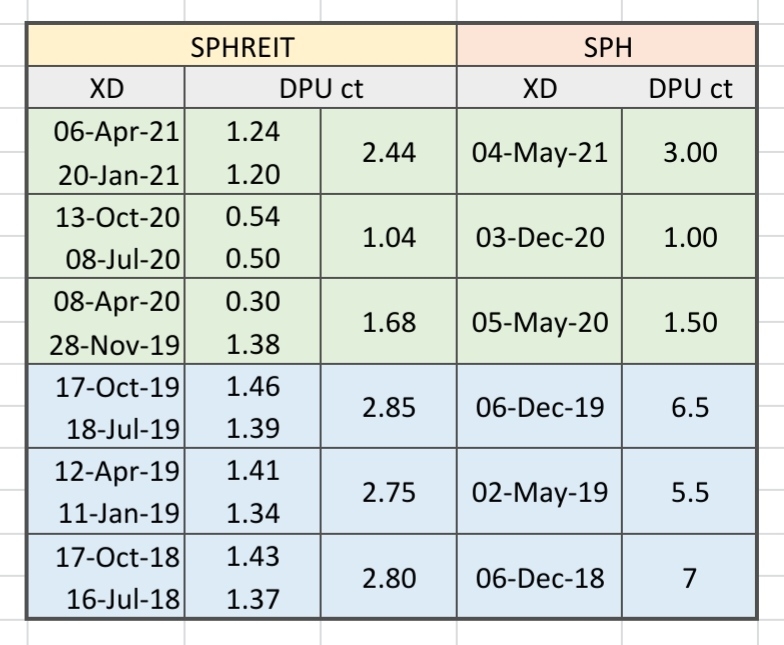

• For a quick projection using SPHREIT DPU trend as reference,

Assuming SPH 2H Div also increase to 3ct (Total 3+3ct),

Yield = 4% @ $1.50 (Current Yield 2.67% @ Div = 1+3 ct)

NAV (after removing Media biz) = $2.08 ie ~25% discount

COMMENTS

• Yield is NOT attractive vs REITs

• Good discount to NAV but likely the norm for Property Co

精彩评论