Amazon is slated to report its fourth-quarter and full-year 2021 results after the market close on Thursday, Feb. 3. An analyst conference call is scheduled for the same day at 5:30 p.m. ET.

The period to be reported on is the second quarter that Andy Jassy has been CEO of the e-commerce and technology giant.

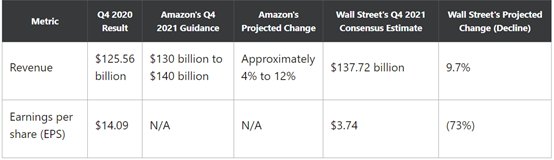

Investors will probably be approaching Amazon's report with some apprehension. Last quarter, the company missed Wall Street's expectations for both revenue and earnings, with the bottom-line miss a sizable one. That was the second consecutive quarter that revenue fell short of the analyst consensus estimate.

Here's what to watch in Amazon's upcoming report.

Amazon's key quarterly numbers

While Amazon doesn't provide guidance for earnings, it does so for operating income. Management expects fourth-quarter operating income to range from $0 to $3 billion, compared with $6.9 billion in the year-ago period. This guidance range represents operating income declining by about 100% to 57% year over year.

The world's e-commerce leader faced tough year-over-year comparables in the fourth quarter. In the year-ago period, revenue surged 44% and earnings per share soared 118% year over year. The fourth quarter of 2020 was particularly strong for two main reasons. First, the pandemic was raging and vaccines had only begun to roll out at the very tail end of the quarter/year. Second, Amazon held its annual Prime Day event in the fourth quarter of 2020 (October), whereas in 2021, this event took place in the second quarter (June).

In last quarter's earnings release, Jassy provided another reason -- increased costs -- that the company's bottom-line results are expected to decline significantly from the year-ago period:

In the fourth quarter, we expect to incur several billion dollars of additional costs in our consumer business as we manage through labor supply shortages, increased wage costs, global supply chain issues, and increased freight and shipping costs -- all while doing whatever it takes to minimize the impact on customers and selling partners this holiday season. It'll be expensive for us in the short term, but it's the right prioritization for our customers and partners.

For context, in the third quarter, Amazon's revenue increased 15% year over year to $110.8 billion, missing the $111.6 billion the Street had expected, but coming in close to the high end of its guidance range of $106 billion to $112 billion. By segment, sales in North America, international, and Amazon Web Services rose 10%, 16%, and 39%, respectively. EPS dropped 51% to $6.12. That result fell considerably short of the analyst consensus estimate of $8.92.

AWS

Through the first nine months of 2021, Amazon's cloud segment, Amazon Web Services (AWS), generated $44.4 billion of revenue while operating at a 30% margin. For one point of comparison, Google Cloud contributed $13.7 billion of revenue for the first nine months of 2021 and is unprofitable, as it reported a loss of $2.2 billion.

What's even more staggering is the pace of AWS's growth. During Q3 2021, AWS generated $16.1 billion of revenue, which represented 39% year-over-year growth. Investors can see that the quarterly operating income of $4.9 billion for the AWS segment was more than Amazon's entire business combined. Amazon Web Services is arguably becoming the most important pillar of the company's ecosystem.

Digital advertising

Amazon has been able to reinvest the profits from its cloud business into other segments, as the company works to differentiate itself from other technology behemoths. One area that is quickly becoming an important crux of Amazon's business is digital advertising.

According to eMarketer, Amazon is expected to comprise 10.7% of the U.S. digital ad market in 2021 and grow to 12.8% by 2023. Although the uptick has been bolstered by increasing consumer reliance on digital shopping during the pandemic, one could argue that this theme will stick because Amazon's platform makes it more time-efficient and cost-effective for consumers to make purchases online versus going to a physical retail location.

The boom on the digital ad side of its business could serve as another lucrative catalyst for the company as it gains market share from Google and Meta Platforms. On the contrary, eMarketer predicts that Google's digital ad business in the U.S. is expected to decrease from 28.9% in 2020 to 26.6% in 2023.

Amazon is well-positioned to benefit from enterprise investment in digital transformation. As the company gains market share over its competition, AWS's capital efficient margin profile will continue fueling additional growth drivers as the company looks to enter new industries.

Prime Membership

Since the pandemic, Amazon has attracted about 30 million new members to its Prime membership program each year (in 2020 and 2021), according to estimates from Consumer Intelligence Research Partners, LLC (CIRP).

Meanwhile, membership renewal rates continued to improve. “The renewal rate after one year hit 94%, while the rate after two years is an impressive 98%, which any other retailer or membership driven business would envy,” said CIRP’s other Partner and cofounder, Mike Levin.

More information from the CIRP report: “As of December 2021, Amazon had 172 million US members. In each of 2020 and 2021, Amazon Prime added about 30 million members in the US. We attribute much of this increase to significantly greater online shopping during the COVID-19 pandemic. This served to accelerate Prime membership growth from slower rates in the previous few years.”

Analysts see upside for the stock in 2022

Earlier this year, BofA analyst Justin Post named Amazon his favorite FAANG stock for 2022, seeing a positive outlook on e-commerce for the next three to five years and growth in Amazon Web Services cloud business.

The stock has zero Sell ratings, three Holds, and 50 Buys or Overweights, according to analysts surveyed by FactSet.

“Though our estimates come down, we believe lower expectations should help de-risk shares and AMZN will become a cleaner story to own through 2022,” J.P. Morgan analyst Doug Anmuth wrote in a research note.

Although Amazon performed well amid a challenging holiday season, Anmuth lowered his first-quarter revenue estimate to $120.5 billion, and trimmed his yearly earnings per share guidance to $75.17, down from $79.47 due to elevated labor, operational, and inflationary costs.

Despite the near-term headwinds, Amazon remains J.P. Morgan’s overall top pick, with Anmuth reiterating his Overweight rating and $4,350 price target.

Revenue should begin to accelerate in the second quarter as costs ease back. Further gains could come as Amazon boosts sales in the grocery, apparel, accessories, and the furniture and appliances sectors, all while selectively increasing prices. Already, the company has raised fulfillment fees by 5%, a move that could add an additional $3 billion in 2022. Anmuth believes Amazon could also hike its Prime membership fees sometime this year.

Amazon also has doubled its fulfillment network and increased its warehouse capacity. Now that the company is no longer space-constrained, it is free to meet elevated demand and invest heavily in marketing, Anmuth said.

Amazon had a tough 2021, gaining just 4% for the year while the S&P 500 rallied 30% —but analysts see upside for the stock in 2022.

精彩评论