- U.S. stock futureswere flat Tuesday.

- On Wall Street, cyclical stocks are the best performers, led by Financials. Info Tech, Communication Services and Energy are slightly lower.

- The dollar and Treasuries yields rose, gold and cryptos dropped.

- Bitcoin could be active today asit becomes legal tender in El Salvador and has gained the attention of the Reddit crowd.

(Sept 7) European bourses dipped in the red and a rally in US equity futures which traded near all-time highs after the Labor Day holiday fizzled, as investors weighed China’s better-than-forecast trade data against the growing likelihood of fading central-bank support. S&P500 futures traded fractionally in the green and Nasdaq 100 indexes slipped and equity gains in China and Japan were followed by losses in Europe as investors speculated the ECB may get ready to roll back stimulus. The dollar and Treasuries yields rose, gold and cryptos dropped.

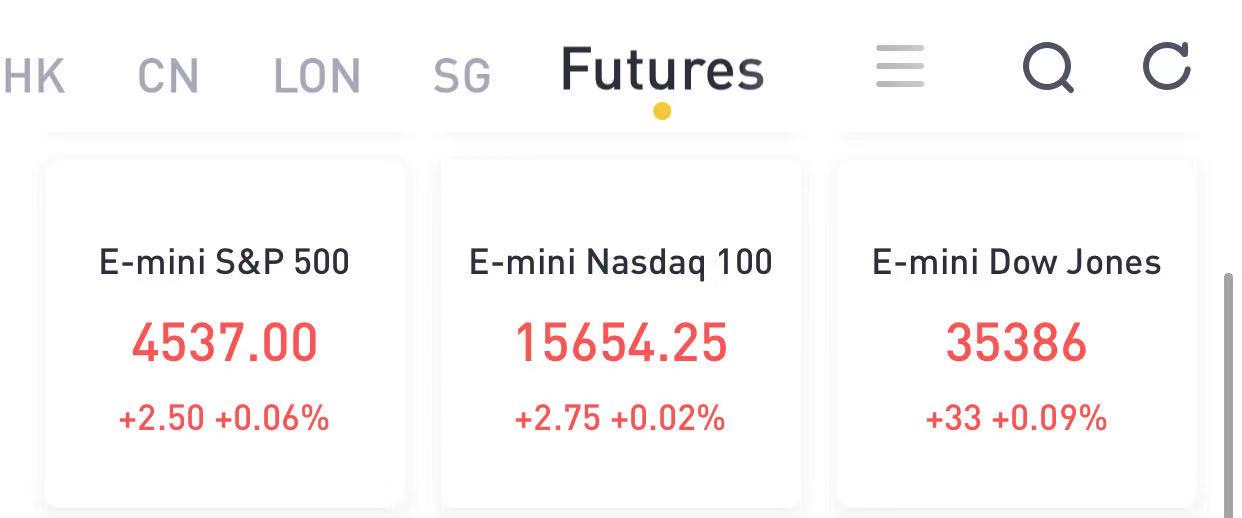

At 8:00 a.m. ET, Dow E-minis were up 33 points, or 0.09%, S&P 500 E-minis were up 2.5 points, or 0.06% and Nasdaq 100 E-minis were up 2.75 points, or 0.02%.

Tech gigacaps such as Microsoft, Amazon.com and Facebook eased about 0.2% each, while Apple and Google were slightly higher.

Tracking benchmark bond yields higher, banks including Wells Fargo, Goldman Sachs, Citigroup and JP Morgan rose between 0.4% and 0.5%.

Among meme stocks, IronNet more than doubled in value in premarket trading after the cybersecurity company was touted on Reddit and StockTwits.

Chinese technology stocks listed in the U.S. rose premarket, amid surprisingly strong trade data (see below), renewed demand for technology shares, the lack of new regulatory announcements and Tencent’s plans to buy back more shares. Alibaba (BABA) was up 2.35% and Didi (DIDI) gained 2.55%, while Baidu (BIDU) gains 3.33%.

Stocks making the biggest moves premarket:

- Alcoa (AA) shares rise 2.9% premarket, catching up with the jump in aluminum prices seen on Monday when U.S. markets were closed.

- Farfetch (FTCH) drops 0.7% after Arete downgraded the stock to sell, citing China risks along with a drag to gross margin from Tmall fees.

- Columbia Property Trust Inc (CXP) jumped 15.8% after Pacific Investment Management Company said it would buy the company for $2.2 billion.

- InflaRx (IFRX) shares rally 23% after it was among the companies awarded grants in Germany for Covid-19 drug development.

- IronNet (IRNT) shares soar 106% with the stock being touted on Reddit and StockTwits.

- Match Group (MTCH) surges 14% on being named to the S&P 500 Index.

- Moderna (MRNA) declines 1.6% after report that Japan’s health ministry said that a man in his 40s died after receiving the biotech’s Covid-19 vaccine from production lots that are being recalled due to possible contamination

- Vertex Pharmaceuticals fell 1.8% in early New York trading after Morgan Stanley cut its stock recommendation to underweight.

The world’s biggest economy remains “in good health” despite a recent increase in Covid-19 infections, according to Mark Haefele, chief investment officer at UBS Global Wealth. “This will support stocks, in our view, especially in cyclical industries like energy and financials,” Haefele said. “We continue to advise investors to position for reopening and recovery.”

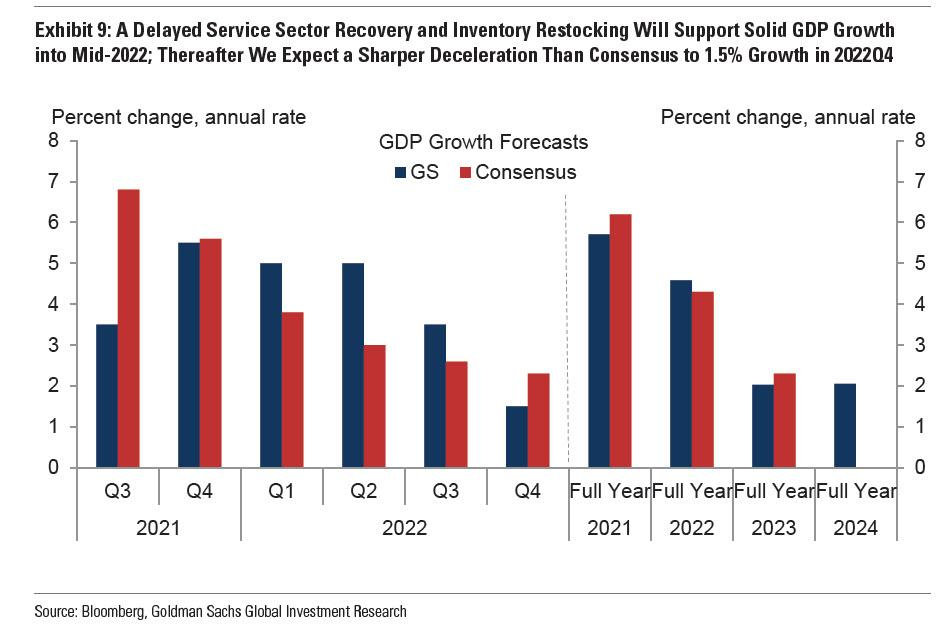

Another thing that supports stocks is that the market is no longer expecting a Fed announcement about tapering in September, Esty Dwek, a global market strategist at Natixis Investment Managers, told Bloomberg Television. “Tapering doesn’t matter that much for markets. It’s priced in, it’s expected. But the reality is that interest rate hikes matter.” Justifying this view wasGoldman's latest GDP forecast cuton Monday, its third in the past month, which saw the bank trim its full-year 2021 GDP forecast to 5.7% from 6.0%.

Optimism that the Fed will delay tapering was offset by concerns that the ECB could turn hawkish at its meeting this week: “There is a growing expectation that the European Central Bank could start talking about tapering its bond purchases sooner rather than later,” Ipek Ozkardeskaya, a senior analyst at Swissquote Group Holdings, wrote in a note. “The ECB hawks who have been in a retreat for the past year won’t stay quiet for longer facing the rising inflation threat.”

Asian stocks climbed, driven by Japanese sharesthat extended a rally after the prime minister’s resignation announcement and a surge in Hong Kong-traded tech names.The MSCI Asia Pacific Index advanced as much as 0.5%, led by the communication-services and consumer-discretionary sectors. Japan’s Nikkei 225 Stock Average briefly broke above the 30,000 level for the first time since April as a reshuffle of the blue-chip gauge added to optimism stoked by potential policy changes that could come under a new national leader. Japanese Finance Minister Aso saidthey will consider compiling a budget with focus on digital, environmental policies, regional economies and ageing population.Furthermore, he doubts if Japan's finances would risk a weaker JPY and inflation, while he suggested it would be good for the next PM to boost government revenue and restrain spending (yes, he really said that).

Adding to the good news was the report that Chinese export growth unexpectedly surged in August, allaying concerns the pandemic is delaying economic reopening and creating supply-chain bottlenecks. China's exports accelerated to 25.6% yoy in August, a sequential rebound of 3.3% in August vs. -0.3% in July. Imports rose 33.1% yoy in August, and grew 2.1% mom sa non-annualized in August (vs. -6.4% in July). Both exports and imports surprised to the upside despite the disruptions to operations at Ningbo port in August due to the local outbreak. Monthly trade surplus rose to $58.3bn in August.

In rates, Treasury yields were cheaper by up to 4bp across 7- to 20-year sectors,with 10-year yields sit around 1.36%, mildly outperforming bunds while gilts trade slightly richer.Treasuries were pressured lower with losses led by intermediates out to long-end ahead of this week’s supply, which kicks off Tuesday with $58b 3-year note sale. Mild risk-on in Asia spurred by China trade data beat saw stocks close higher and Treasuries trade heavy, adding to auction concessions. U.S. auction cycle includes 10- and 30-year offerings Wednesday and Thursday. Peripheral spreads have a marginal tightening bias to core; Spain underperformed slightly with focus today on issuance of the sovereign’s inaugural green bond.

In commodities, crude futures drift within Monday’s trading range. WTI hovers near $69. Brent near $72.50. Spot gold drops ~$10 to trade near $1,813/oz. LME copper underperforms peers with a 1% decline.

精彩评论