Beyond Meaton Thursday reported a wider-than-expected loss in the first quarter as restaurant customers take longer to return and grocery shoppers aren’t stockpiling its meat substitutes anymore.

However, CEO Ethan Brown said the company is seeing a “slow thaw” in its food service segment in the United States and some international markets, prompting the company to issue a revenue forecast for the next quarter.

Shares of the company fell 6.7% in extended trading.

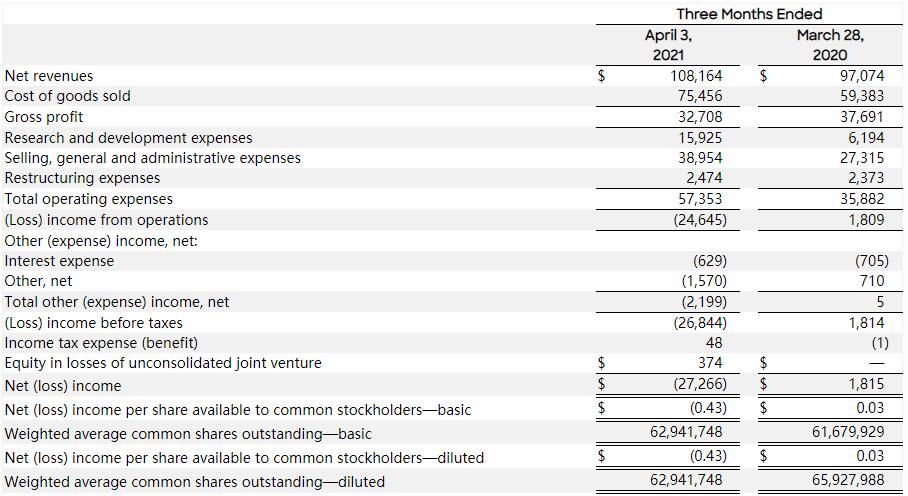

- Loss per share: 42 cents adjusted vs. 19 cents expected

- Revenue: $108.2 million vs. $113.7 million expected

Beyond reported fiscal first-quarter net loss of $27.3 million, or 43 cents per share, down from net income of $1.8 million, or 3 cents per share, a year earlier.

This is the third quarter in a row that Beyond has reported a wider-than-expected loss. The company has been investing back into its business as it tries to position itself as a global player. Beyond now has production facilities in China and the Netherlands, for example.

Net salesrose 11.4% to $108.2 million, missing expectations of $113.7 million.

U.S. retail sales jumped by 27.8% during the quarter. Sales in grocery and convenience stores accounted for more than three-quarters of the company’s total U.S. revenue. Prior to the pandemic, retail sales made up only about half of Beyond’s revenue.

Food service sales in the U.S. fell 26% as streamlined menus and less customer traffic at restaurants hurt demand. Beyond also lost roughly 3,000 foodservice locations, which the company attributed to the pandemic. Brown said that the company has added about 2,400 locations since the quarter ended.

Rival Impossible Foodshas been slashing prices of its meat substitutes, helping it toward its goal of achieving price parity with beef. According to Brown, the move hasn’t pulled many customers away from Beyond’s products, which he said shows strong brand loyalty.

“We just did some comparative data analysis, and we looked at their consumer and our consumer and take-away and things of that nature, and what’s really interesting is while they’re doing a really good job building the category and bringing people into the category, they’re not sourcing a lot of our consumers,” Brown said.

Outside of Beyond’s home market, sales rose 12.5%, fueled by skyrocketing retail demand. International grocery sales nearly tripled during the quarter. In total, international sales account for a quarter of the company’s revenue, and Beyond’s meat substitutes are sold in more than 80 countries worldwide.

For the second quarter, the company is forecasting revenue in the range of $135 million to $150 million, representing an increase of 19% to 32% compared with the year-ago period. Wall Street analysts are expecting net sales of $142.8 million next quarter. Executives said that the company did not include a significant uptick in its foodservice sales in the forecast.

Brown said that the company will revisit the outlook if there’s a significant resurgence of Covid-19 in the U.S. or other important markets.

Beyond did not provide an outlook for the full year, citing the uncertainty caused by the pandemic.

CFO Mark Nelson retired Wednesday, which was previously announced. Brown said that the company will reveal his successor in the coming weeks.

精彩评论